Abstract

Foreign Exchange Reserves of the countries play a major role in managing exchange rate and monetary policy, particularly in emerging countries as Sri Lanka. Therefore, it is important to manage foreign exchange reserves in an open and transparent manner with clear objectives of what is going to be achieved. For a country like Sri Lanka the main objective would be the safety of the assets since it is difficult to absorb substantial risks in managing foreign exchange reserves due to relative lower size compared to its exposure to external sector of the economy. When it comes to gold as an assets class is considered to safe-haven assets due to its nature of higher return in times of crisis and inflationary periods. The objective of this study is to explore the diversification impact of gold on foreign exchange reserves in Sri Lanka for the period from 2007 to 2023. To explore the impact of diversification, correlation between gold and existing foreign exchange reserves and additional excess return per unit of risk provide with the inclusion of gold into the portfolio were used to analyze the possible diversification impact. The results showed that there is an increase in excess return with the addition of 1% to 5% of gold as a percentage of total foreign exchange reserves, while correlation of gold with existing portfolio was less than 0.5 indicating diversification impact. Further, the Sharpe ratio was also seen increasing when the gold composition in foreign exchange reserve portfolio was increased. It was found that gold can be considered as an asset class which help diversification for foreign exchange reserves of Sri Lanka, even though the same are managed in very conservatively.

Keywords

Foreign Exchange Reserves, Diversification, Correlation, Sharpe Ratio

1. Introduction

Most of the countries in the world (one hundred and eight as at March 2024) have some portion of their foreign exchange reserves in terms of gold due to various reasons such as legacy holdings (existing positions), as a long-term store of value, hedge against in times of crisis, no default risk in the case of physical gold, effectiveness of the diversification impact.

As per the data compiled by World Gold Council, Central Banks around the world hold around 17% of the estimated mined gold as at end 2023. Since gold as physical asset last long, almost all the gold which was mined is still available in different form around the world.

These days, the term foreign exchange reserve asset is commonly linked to cash deposits in foreign currencies and highly liquid tradable instruments, such as bills, notes, and bonds issued by the US Treasury or other highly rated government entities. Interestingly, and somewhat unusual by today's standards, the Balance of Payment Manual of International Monetary Fund (IMF) list of foreign exchange reserve assets places monetary gold as the first component of reserves.

A substantial amount of literature has discussed gold's properties as a diversifying asset. This topic was popular in the 1980s regarding developed economy equity markets

| [7] | Chua, J. H., Sick, G., & Woodward, R. S. (1990). Diversifying with gold stocks. Financial Analysts Journal, 46(4). (1990), 76–79. https://doi.org/10.2469/faj.v46.n4.76 |

| [13] | Herbst, A F “Gold versus U.S. common stocks: some evidence on inflation hedge performance and cyclical behavior”, Financial Analysts Journal, vol 39(1). (1983), pp 66-74. |

[7, 13]

and has recently gained attention in the context of emerging markets, such as China

and the BRICS nations

| [6] | Chkili, W Dynamic correlations and hedging effectiveness between gold and stock markets: Evidence for BRICS countries, Research in International Business and Finance, Volume 38. 2016. https://doi.org/10.1016/j.ribaf.2016.03.005 |

[6]

.

In the context of foreign exchange reserves, analyses of gold's potential value in fixed income and multi-asset portfolios are particularly relevant. Jaffe

| [16] | Jaffe, J. F. Gold and gold stocks as investments for institutional portfolios. Financial Analysts Journal, 49(2). (1989), 53–59. |

[16]

investigated the risk-return characteristics of gold in portfolios with varying risk appetites, each represented by different combinations of stocks and bond portfolios. He learned that including 5% to 10% of gold can improve the Sharpe ratio of the portfolio. An extended study done by Emmrich and McGroarty

| [10] | Emmrich, O and F J McGroarty “Should gold be included in institutional investor portfolios?”, Applied Financial Economics, 23: 19. (2013), pp 1553-1565. |

[10]

, which contains a wide literature review, recommended a 10% gold allocation, emphasizing gold's role in balancing equity exposures. Moreover, the well-known analysis by Bauer and Lucey

studied whether gold can function as a safe-haven in the stock and bond markets of the USA, the UK, and in Germany. Their findings indicated that gold may not always serve as a safe-haven for stocks and bonds.

A major shortcoming of the above-mentioned studies is their focus was mainly on equity markets, from reserve management perspectives, main focus is on investing in fixed income securities due to frequent liquidity requirements of foreign exchange reserve portfolios and relatively lower level of risk tolerance.

As per the annual report of Central bank of Sri Lanka (CBSL), in 2016 foreign reserve management strategy has changed to a more scientific method called Strategic Assets Allocation (SAA) after joining the Reserve Advisory and Management Programme (RAMP) of the World Bank with the objective of gaining enhanced technical expertise in Reserve Management

| [4] | Central Bank of Sri Lanka, Annual Reports 2016, Central Bank of Sri Lanka, Colombo, 2017. |

[4]

. Under the new approach CBSL has managed the FX reserves which permits assets to be allocated according to the liability structure. Therefore, there is a future research opportunity to explore the value addition of new approach and quantify the effectiveness of SAA approach yielded to foreign reserve function of Sri Lanka.

Objective of the Study

This study’s contribution is on filling the gap in research work related to foreign exchange reserve management in Sri Lanka on analysis on diversification effect of gold as an asset class, with an analysis on excess returns, Sharpe ratios, correlation impact typically associated with foreign exchange reserves portfolio as almost all, except gold holding, foreign exchange reserves of Sri Lanka has been invested in fixed income securities. The author did not find any literature on the selected area of study has been done previously as this is the first time an analysis on foreign exchange reserves is conducted, may be due to data are not readily available and available data need to be adjusted to suit the analysis.

Scope of the Study

The impact on diversification from addition of gold to any portfolio needs to be analyzed by removing the impact of gold already included in the existing portfolio. The scope of the study was on removing return earned from average gold holding during a year and adding predetermined gold percentage to ex gold foreign exchange reserves portfolio, due to limitation of publicly available data. The period covered under the study was started from 2007 to end 2023 with annual return data of foreign exchange reserves and all other information was also obtained with annual frequency in order to be consistent data collected for the study. To measure the effect of diversification correlation, Sharpe ratio and excess returns were used in this study.

Limitation of the Study

The frequency of the data collection was only on annual due to non-availability of financial statements of Central Bank of Sri Lanka, who manages the foreign exchange reserves of the country. If more frequent data collected (monthly or quarterly,) the data series would have been more in line with actual data in the case of foreign exchange reserves return. The same limitation applies to the gold return portion as exact return earned from gold may have slight differences from the return calculated under this study. However, both gold and foreign exchange reserves return was calculated using annual data series these differences may be set off against each other, leading to lesser deviation.

2. Literature Review

Investments in gold can be done in few different ways, including investing in physical gold, paper gold which track the spot prices of the physical gold prices, via Exchange Traded Funds, or gold pooled accounts. Except while holding physical gold, investor must bear the risk of the counterparty even though the investment tracks the prices of gold, as there may not be actual holding backed for other kinds of investments in gold exposure. When compared to investments like equity, bonds, physical gold does not carry any credit risk as it is not the liability of any issuer and has a physical asset to hold.

Diversification effect of Gold Vs Various assets classes

The impact on risk management in portfolio of gold was analyzed

for multi assets portfolio and found that gold can help to have low correlation with existing portfolio and gold can potentially helped to lower portfolio volatility and thus, if all other factors are being equal, it will increase the diversification by enhancing overall risk adjusted return, it was found that low correlation existed over a longer period like 30 years

.

Usually in a time of crisis, even though there are diversification benefit holding certain types of assets, many assets become increasingly highly correlated with the increase in volatility

eventually reducing the diversification benefit which was expected at the time of investment made. Further, it was found that Gold has become increasingly easy to sell during the time of turbulence unlike other assets where usually difficult to find a prospective buyer even at lower prices

| [11] | Fernando, N. Shalinda. “The Role of Gold in an Investment Portfolio: An empirical study on diversification benefits of gold from the perspective of Swedish investors.” (2017). https://api.semanticscholar.org/CorpusID:169010890 |

| [8] | Conover, C. M., Jensen, G. R., Johnson, R. R., & Mercer, J. M. Is now the time to add commodities to your portfolio? The journal of Investing, 19(3). (2010), 10-19. |

[11, 8]

.

Bank for International Settlement (BIS) working paper done by Zulaica

, found that relatively more important finding for emerging market economy like in the case for Sri Lanka, where it was stated that for countries which have high foreign exchange risks, inclusion of gold provides enhanced benefits for diversification and showed that gold holding up to 20% would be as optimal portfolio allocation.

Further, Zulaica,

in his paper found that benefits that accrue from gold as a hedge in extreme tail event situations, are high for the longer duration holding period with high gold allocation as 20% to 50%. Further, it was found that selecting an adequate share of gold for the foreign exchange reserves portfolio is dependent on policy objectives and risk tolerance level of the portfolio.

Dempster,

| [9] | Dempster, N., & Artigas, J. C. Gold: Inflation hedge and long-term strategic asset. The Journal of Wealth Management, 13. (2010), 69-75. |

[9]

examined the gold as inflation hedge and as a long terms’ strategic asset with the data during the period from 1974 to 2008, found that gold has outperformed in the years where there were periods with high inflation against with other assets classes like bonds, equities, and even with other commodities.

Gold as a reserve asset

Gold holdings in their foreign exchange reserves have analyzed by Zulaica,

, and observed that advanced economies hold relatively higher percentage of gold holding in their portfolio, which is around 20% by 2020, while emerging economies hold comparatively lesser amount of gold in their portfolio with an average of 7.4% by 2020. The overall trend had seen a downward trend until 2006 and thereafter saw some oscillations up until 2020. according to the World Gold Council,

gold holding remained at an average of 17% of total foreign exchange reserves around the world, suggesting that still countries have appetite to hold significant fraction of foreign exchange reserves as gold.

Gold as Safe haven asset

Several studies have been done to identify the concept of safe-haven asset without any indication to gold but, Nusantara,

has done a study to see the if gold is a safe-haven asset or not. The result indicated that there was no evidence to consider gold as safe-haven, with regard to movement of international prices and further Baur and Lucey

also found no evidence for gold act as haven assets against bonds. However, there was negative correlation between US dollar and gold prices during the period from 2013 to 2020 as evidenced by Nusantara

, indicating gold as hedge instruments against US dollar, confirmed by Capie et al.,

| [3] | Capie, F., Mills, T. C., & Wood, G. Gold as a hedge against the dollar. Journal of International Financial Markets, Institutions and Money, 15(4). (2015), 343-352. |

[3]

. Conversely, some researchers found that gold exhibits signs of safe-haven assets, which are hedging properties during a times of crisis Pullen et al,

| [19] | Pullen, T., Bensen, K., & Faff, R. A comparative analysis of the investment characteristics of alternative gold assets. Abacus, 50. (2014), 76–92. https://doi.org/10.1111/abac.12023 |

[19]

, and Baur and Lucey

.

The author’s view is that more research to be done in analyzing safe-haven assets features of gold as the empirical study’s findings are not conclusive due to some researcher may have mis understood or mix up the two concept of diversification and safe-haven features.

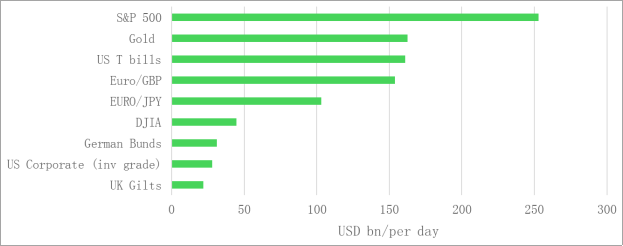

Liquidity of Gold market

Figure 1. Average Daily volumes of different markets in 2023.

The majority of average daily volume of gold trades are done through over the counter markets (61%) while 38% of trades are done through various global exchanges and gold Exchange Traded Funds also had a daily average volume of USD 2 bn in 2023

. As per

figure 1, shown above, the gold market has fairly high liquidity level compared to selected major financial markets and assets. The liquidity of gold markets is large enough to accommodate institutional investors. In contrast, to financial markets, at times of financial crisis, liquidity of gold market doesn’t dry up which allows investors to meet the liability in situations where other assets are illiquid

.

Impact of Gold on Portfolio volatility

The impact of gold on volatility of overall portfolio can be looked at in two aspects. The first aspect had looked at by Zulaica,

by comparing volatility of different currencies over a given period then compared the volatility of the same currencies after inclusion of gold, where it was found that currencies with higher volatility had lower impact to volatility with inclusion of gold. In contrast, currencies which had lower volatility or lower exposure to exchange rate risk are less sensitive to increased gold allocations.

State Street,

analyzed gold weekly return for the period from 1990 to 2023 and compared volatility of equity, fixed income securities volatility and currency volatility. The relevant indexes are used to measure the volatility of each category. It was found that gold has helped to mitigate the risk arising from equity market drawdowns and volatility caused due to technical and sudden spikes in volatility. When there is high volatility in the US treasury markets and foreign exchange markets, gold average weekly performance was turned to be positive and was able to outperform the assets classes like Bonds and currencies.

3. Methodology

The methodology adopted by Hoang et al.,

| [15] | Hoang, T, et al; Is gold good for portfolio diversification? A stochastic dominance analysis of the Paris stock exchange, International Review of Financial Analysis. (2015). |

[15]

has used in this study to explore the diversification effect on gold investments in foreign exchange reserves portfolio of Sri Lanka for the period from 2007 to 2023. The total and excess return of the foreign exchange reserves calculated removing the estimated gold return, which was already included, and the same was compared against the new portfolios created by adding 1% to 5% of gold return to see whether there is any additional return derived from the addition of gold to the existing foreign exchange reserves portfolio. Further, in order to see the contribution of risk adjusted by inclusion of gold also was checked by Hoang et al.,

| [15] | Hoang, T, et al; Is gold good for portfolio diversification? A stochastic dominance analysis of the Paris stock exchange, International Review of Financial Analysis. (2015). |

[15]

with comparing Sharpe ratio of different portfolios.

Sample period

The sampling period was 2007 to 2023 with annual data collected from the public sources used for the analysis.

Variables and formulas

Rate of return (Rp)

Where:

V1 = Value of the portfolio at the end

V0 = Value of the portfolio at the beginning

Risk (Standard Deviation)

Excess Return (ER)

Where:

Rf = Risk free rate

Correlations coefficient (r)

Where:

Sharpe Ratio

(5)

Where: Standard Deviation of excess return

Benchmark Return – US 10 Year yield

b(6)

Foreign Exchange Reserve Portfolio Annual Return

(7)

Gold Return

(8)

Foreign Exchange Reserve Portfolio Annual Return excluding the return from gold (Ex Gold Return)

(9)

4. Results and Discussions

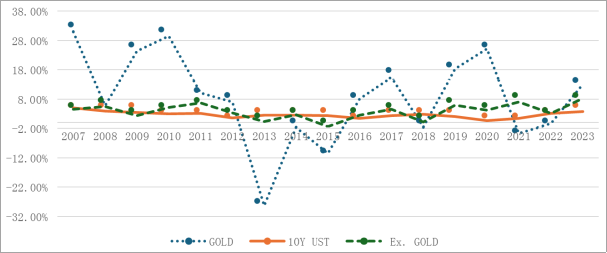

The analysis of each portfolio returns over the period from 2007 to 2023 is shown below in

Figure 2 Performance of FX Reserve (Ex Gold) Vs 10Y UST and Gold. The initial indication from the

figure 2 signals that there could be an additional return opportunity from adding gold to foreign exchange reserves portfolio due to volatility in the gold return with comparatively higher level of returns during the period under study. Further looking at overall annual average return of foreign exchange reserves portfolio excluding gold have recorded 3.79% over 17 years period has comfortably been outperformed by gold return during the same period by earning an 8.38%. The question now would be whether there is sufficient correlation between two variables to have a return benefit by adding gold to the existing portfolio. The calculated figure of correlation of 0.46, which is less than half suggests that the existence of diversification benefits.

Figure 2. Performance of FX Reserve (Ex Gold) Vs 10Y UST and Gold.

Since the above analysis shows additional return potential by addition of a certain percentage of gold to existing portfolio, the excess return that could have earned was analyzed as per

Table 1. The benchmark which was used is return of US Treasury 10-year bond which is very liquid instrument can be replicated easily due to higher liquidity, lower bid-ask spread order book impact Fleming

.

The excess return earned was analyzed by creating four additional portfolios by adding 1%, 2%, 3%, 5% to existing foreign exchange reserves portfolio (Ex Gold). The same five portfolios are used in the entire analysis of this paper for the analysis.

As per the results of

Table 1, excess return earned over the benchmark had improved during the period covered in the study and the excess return earned has increased in line with the increase in gold allocation to existing portfolio.

Table 1. Excess Return over the Benchmark.

| Excess Return over the Benchmark |

Year | Ex. GOLD2 | GOLD 1% 2 | GOLD 2% | GOLD 3% | GOLD 5% |

2007 | -0.49% | -0.23% | 0.04% | 0.30% | 0.83% |

2008 | 1.60% | 1.60% | 1.60% | 1.61% | 1.61% |

2009 | -1.60% | -1.38% | -1.15% | -0.93% | -0.48% |

2010 | 1.76% | 2.01% | 2.26% | 2.51% | 3.00% |

2011 | 3.51% | 3.54% | 3.58% | 3.61% | 3.68% |

2012 | 1.86% | 1.89% | 1.93% | 1.96% | 2.03% |

2013 | -2.03% | -2.32% | -2.61% | -2.90% | -3.47% |

2014 | 0.12% | 0.08% | 0.04% | 0.00% | -0.08% |

2015 | -3.73% | -3.82% | -3.91% | -4.00% | -4.18% |

2016 | 1.09% | 1.15% | 1.20% | 1.26% | 1.37% |

2017 | 2.29% | 2.39% | 2.50% | 2.61% | 2.83% |

2018 | -2.62% | -2.64% | -2.66% | -2.68% | -2.71% |

2019 | 3.75% | 3.87% | 4.00% | 4.12% | 4.38% |

2020 | 3.46% | 3.67% | 3.88% | 4.09% | 4.51% |

2021 | 5.63% | 5.52% | 5.41% | 5.30% | 5.09% |

2022 | 0.00% | -0.03% | -0.07% | -0.10% | -0.17% |

2023 | 4.51% | 4.56% | 4.61% | 4.66% | 4.75% |

As depicted in

Table 2, the excess return has reported high as 5.09% with reporting higher average return of 1.35% (Gold 5%) in the same portfolio. When compared to mean return during the period, has reported an improvement with the addition of gold, irrespective of the percentage of gold added.

Table 2. Excess Return Descriptive Statistics.

| Excess Return |

Ex. GOLD | GOLD 1% | GOLD 2% | GOLD 3% | GOLD 5% |

Lowest | -3.73% | -3.82% | -3.91% | -4.00% | -4.18% |

Mean | 1.12% | 1.17% | 1.21% | 1.26% | 1.35% |

Highest | 5.63% | 5.52% | 5.41% | 5.30% | 5.09% |

The cumulative total return and excess return also analyzed to see the contribution of excess return to the total return over total time horizon and it was found that there is 31% to 34% contribution from excess return over the benchmark to total return earned during the period. This is in comparison to the 29% excess return ratio earned with the existing portfolio.

Table 3. Return and Excess Return of different portfolios.

Description | Ex. GOLD | GOLD 1% | GOLD 2% | GOLD 3% | GOLD 5% |

Total Return | 65% | 65% | 66% | 67% | 68% |

Excess Return | 19% | 20% | 21% | 21% | 23% |

Excess Return/Total Return | 29% | 31% | 32% | 31% | 34% |

The correlation analysis reflects the existence of diversification benefits with varying level once the gold exposure was included into the existing foreign exchange reserves portfolio, as the correlation between two portfolios are less than positive one, in the range of 0.55 to 0.56 (

Table 4) indicating relatively substantial diversification benefits. In contrast to correlation exist between foreign exchange reserves portfolio and adding 1% to 5% of gold into total portfolio, correlation between UST 10Y benchmark and gold was reported very low positive figures compared to existing foreign exchange reserves and gold. The reason may be due to a foreign exchange reserves portfolio consisting not only US dollar denominated instruments but also other currencies

| [5] | Central Bank of Sri Lanka, Annual Reports 2020, Central Bank of Sri Lanka, Colombo, 2021. |

[5]

.

Table 4. Correlation Matrix.

| FX Reserve | UST 10Y |

Gold 1% | 0.55 | 0.22 |

Gold 2% | 0.56 | 0.16 |

Gold 3% | 0.56 | 0.16 |

Gold 5% | 0.56 | 0.18 |

The above analysis suggested the strong case of diversification effect of gold inclusion to existing foreign exchange reserves portfolio, therefore further analysis was done to quantify the diversification impact of gold as an asset class.

By using the mean variance analysis, Sherman

has concluded that gold has generated positive excess return and using Sharpe ratio/ risk reward ratio Hillier et al.

found that gold improved the performance of existing equity investment portfolio. As per the analysis in below

Table 5 and

Table 6, for 17 years period from 2007 to 2023, foreign exchange reserves portfolio has been able to generate additional risk adjusted return per unit of risk in various gold exposure added to existing portfolio.

Over the period of analysis, it was noted that the Sharpe ratio increased when 1% to 5% gold is included in the existing foreign exchange reserve portfolio, which means return per unit of risk increases in almost all the cases. While in some cases either increase in Sharpe ratio is low or marginal negative due to higher volatility that might have experienced respective year. Hence including gold in the FX reserve portfolio improves its performance against risk free assets return.

Table 5. Excess Return per unit of risk for different portfolios.

| Sharpe Ratio |

Year | Ex. GOLD | GOLD 1% | GOLD 2% | GOLD 3% | GOLD 5% |

2007 | (0.20) | (0.09) | 0.02 | 0.12 | 0.33 |

2008 | 0.64 | 0.64 | 0.64 | 0.64 | 0.65 |

2009 | (0.64) | (0.55) | (0.46) | (0.37) | (0.19) |

2010 | 0.71 | 0.80 | 0.90 | 1.00 | 1.20 |

2011 | 1.41 | 1.42 | 1.43 | 1.45 | 1.47 |

2012 | 0.74 | 0.76 | 0.77 | 0.79 | 0.81 |

2013 | (0.81) | (0.93) | (1.05) | (1.16) | (1.39) |

2014 | 0.05 | 0.03 | 0.02 | 0.00 | (0.03) |

2015 | (1.49) | (1.53) | (1.56) | (1.60) | (1.67) |

2016 | 0.44 | 0.46 | 0.48 | 0.50 | 0.55 |

2017 | 0.92 | 0.96 | 1.00 | 1.05 | 1.13 |

2018 | (1.05) | (1.06) | (1.06) | (1.07) | (1.09) |

2019 | 1.50 | 1.55 | 1.60 | 1.65 | 1.75 |

2020 | 1.38 | 1.47 | 1.55 | 1.64 | 1.81 |

2021 | 2.25 | 2.21 | 2.17 | 2.12 | 2.04 |

2022 | 0.00 | (0.01) | (0.03) | (0.04) | (0.07) |

2023 | 1.81 | 1.83 | 1.85 | 1.86 | 1.90 |

Further, as per the table below, mean Sharpe ratio also has seen a significant improvement in its performance in the range of 4% to even high as 20% which is significant as the Sharpe ratio calculates the excess return per unit of risk. When the gold included highest Sharpe ratio reported was lower than that of existing portfolio due to higher volatility of gold in years where there was a negative return, which can be minimized in the long run as evidenced in this analysis supporting strong case of diversification effect of gold as confirmed with their studies by Hoang et al.,

| [15] | Hoang, T, et al; Is gold good for portfolio diversification? A stochastic dominance analysis of the Paris stock exchange, International Review of Financial Analysis. (2015). |

[15]

and Fernando

.

Table 6. Descriptive Statistics of Sharpe Ratio.

| Sharpe Ratio |

Ex. GOLD | GOLD 1% | GOLD 2% | GOLD 3% | GOLD 5% |

Lowest | (1.49) | (1.53) | (1.56) | (1.60) | (1.67) |

Median | 0.64 | 0.64 | 0.64 | 0.64 | 0.65 |

Mean | 0.45 | 0.47 | 0.49 | 0.50 | 0.54 |

Highest | 2.25 | 2.21 | 2.17 | 2.12 | 2.04 |

5. Conclusion

The one of the main objectives of foreign exchange reserve management is to diversify its portfolio to manage the risk while earning stable return meeting foreign exchange liquidity needs of the country. The correlation among assets class like bonds and equity are rising which result in shrinking diversification benefits. Therefore, portfolio managers/central banks are forced to look for alternative asset classes to include in their portfolio increase return while keeping the risk at tolerable level.

This study was done to explore the effect on diversification of foreign exchange reserve portfolio of Sri Lanka by adding 1% to 5% gold exposure with the data collected from 2007 to 2023 using the public sources and data bases maintained internationally.

The analysis revealed that selecting an adequate share of gold is important and depends on risk tolerance level of the portfolio as gold provides diversification benefits with increased level of volatility as suggested by the Sharpe ratio analysis done in this study. However, there is a possible protection against adverse scenarios

| [17] | Nugee, J “Foreign Exchange Reserves Management”, Bank of England. (2000). |

[17]

. Therefore, as suggested by Zulaica,

, careful risk return analysis needs to be supplemented by qualitative analysis for foreign exchange reserve portfolio for deciding the optimal allocation of gold, which is beyond the scope of this study.

The results of the study showed that improvement in excess return on average is in the range of 5 basis points to 23 basis points

which is substantial considering the average absolute return earned during the period under study of below 2%. Therefore, gold has shown significant potential for improvement in excess return of foreign exchange reserves. Since the excess return enhancement was significant, further analysis was done to explore the impact of gold in risk adjusted return as correlation between gold and existing portfolio, was around 0.5. Since the Sharpe ratios of all the portfolios reported positive and increase in ratio when the gold allocation was increased, the tested hypothesis in this study of diversification of gold as an asset class was able to demonstrate in the case of foreign exchange reserve portfolio of Sri Lanka.

Further, as future research study, one can explore the optimum level of gold allocation in foreign exchange reserves portfolio for countries like Sri Lanka and to generalize the same for emerging market countries with lower middle-income levels.

Abbreviations

Ex Gold | Foreign Currency Reserve Excluding Gold |

GOLD | Gold Index |

FX Reserve | Foreign Currency Reserve Portfolio |

Bps | Basis Points |

UST 10Y | US Treasury 10-Year Yield |

Author Contributions

Roshan Harshapriya is the sole author. The author read and approved the final manuscript.

Data Availability Statement

The data that support the findings of this study can be found at:

https://www.cbsl.gov.lk/en/publications/economic-and-financial-reports/annual-reports and;

https://www.gold.org/goldhub/data/gold-prices and.

https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

Funding

This work is not supported by any external funding.

Conflicts of Interest

The author declares no conflicts of interest.

References

| [1] |

Arouri M. H, Lahiani, D. K. Nguyen World gold prices and stock returns in China: insights for hedging and diversification strategies Econ. Model., 44(2015), pp. 273-282.

https://doi.org/10.1016/j.econmod.2014.10.030

|

| [2] |

Baur, D. G., Lucey, B. M. Is gold a hedge or a safe haven? An analysis of stocks, bonds, and gold. The Financial Review, 45. (2010), 217–229.

https://doi.org/10.1111/j.1540-6288.2010.00244.x

|

| [3] |

Capie, F., Mills, T. C., & Wood, G. Gold as a hedge against the dollar. Journal of International Financial Markets, Institutions and Money, 15(4). (2015), 343-352.

|

| [4] |

Central Bank of Sri Lanka, Annual Reports 2016, Central Bank of Sri Lanka, Colombo, 2017.

|

| [5] |

Central Bank of Sri Lanka, Annual Reports 2020, Central Bank of Sri Lanka, Colombo, 2021.

|

| [6] |

Chkili, W Dynamic correlations and hedging effectiveness between gold and stock markets: Evidence for BRICS countries, Research in International Business and Finance, Volume 38. 2016.

https://doi.org/10.1016/j.ribaf.2016.03.005

|

| [7] |

Chua, J. H., Sick, G., & Woodward, R. S. (1990). Diversifying with gold stocks. Financial Analysts Journal, 46(4). (1990), 76–79.

https://doi.org/10.2469/faj.v46.n4.76

|

| [8] |

Conover, C. M., Jensen, G. R., Johnson, R. R., & Mercer, J. M. Is now the time to add commodities to your portfolio? The journal of Investing, 19(3). (2010), 10-19.

|

| [9] |

Dempster, N., & Artigas, J. C. Gold: Inflation hedge and long-term strategic asset. The Journal of Wealth Management, 13. (2010), 69-75.

|

| [10] |

Emmrich, O and F J McGroarty “Should gold be included in institutional investor portfolios?”, Applied Financial Economics, 23: 19. (2013), pp 1553-1565.

|

| [11] |

Fernando, N. Shalinda. “The Role of Gold in an Investment Portfolio: An empirical study on diversification benefits of gold from the perspective of Swedish investors.” (2017).

https://api.semanticscholar.org/CorpusID:169010890

|

| [12] |

Fleming, M How Has Treasury Market Liquidity Evolved in 2023, Federal Reserve Bank of New York, 2023,

https://libertystreeteconomics.newyorkfed.org/2023/10/how-has-treasury-market-liquidity-evolved-in-2023/

|

| [13] |

Herbst, A F “Gold versus U.S. common stocks: some evidence on inflation hedge performance and cyclical behavior”, Financial Analysts Journal, vol 39(1). (1983), pp 66-74.

|

| [14] |

Hillier, D., Draper, P., & Faff, R. Do precious metals shine? An investment perspective. Financial Analysts Journal, vol. 62, no. 2. (2006), 98-106.

https://doi.org/10.2469/faj.v62.n2.4085

|

| [15] |

Hoang, T, et al; Is gold good for portfolio diversification? A stochastic dominance analysis of the Paris stock exchange, International Review of Financial Analysis. (2015).

|

| [16] |

Jaffe, J. F. Gold and gold stocks as investments for institutional portfolios. Financial Analysts Journal, 49(2). (1989), 53–59.

|

| [17] |

Nugee, J “Foreign Exchange Reserves Management”, Bank of England. (2000).

|

| [18] |

Nusantara, Agung & Nawatmi, Sri & Santosa, Agus & Sudiyatno, Bambang The Role of Gold as Haven or Diversifier Investment in Indonesia.

https://doi.org/10.21203/rs.3.rs-789580/v1

(2021).

|

| [19] |

Pullen, T., Bensen, K., & Faff, R. A comparative analysis of the investment characteristics of alternative gold assets. Abacus, 50. (2014), 76–92.

https://doi.org/10.1111/abac.12023

|

| [20] |

Sherman, E. J. (1982, Spring). Gold: A conservative, prudent diversifier. The Journal of Portfolio Management, (1982) 21–27.

https://doi.org/10.3905/jpm.1982.408850

|

| [21] |

State Street, Invest in Gold A portfolio Diversifier with Staying power, white paper State Street (2024).

https://www.ssga.com/library-content/products/fund-docs/etfs/us/insights-investment-ideas/spdr-invest-in-gold.pdf

|

| [22] |

World Gold Council, Gold as a strategic asset: 2024 edition. (2024),

https://www.gold.org/goldhub/research/relevance-of-gold-as-a-strategic-asset

|

| [23] |

Zulaica, O What share for gold? On the interaction of gold and foreign exchange reserve returns, BIS working paper, (2020).

https://www.bis.org/publ/work906.pdf

|

Cite This Article

-

APA Style

Harshapriya, R. (2024). Diversification Effect of Gold as an Asset Class in Foreign Exchange Reserve Portfolio, Evidence from Sri Lanka. International Journal of Economics, Finance and Management Sciences, 12(5), 267-275. https://doi.org/10.11648/j.ijefm.20241205.14

Copy

|

Copy

|

Download

Download

ACS Style

Harshapriya, R. Diversification Effect of Gold as an Asset Class in Foreign Exchange Reserve Portfolio, Evidence from Sri Lanka. Int. J. Econ. Finance Manag. Sci. 2024, 12(5), 267-275. doi: 10.11648/j.ijefm.20241205.14

Copy

|

Download

AMA Style

Harshapriya R. Diversification Effect of Gold as an Asset Class in Foreign Exchange Reserve Portfolio, Evidence from Sri Lanka. Int J Econ Finance Manag Sci. 2024;12(5):267-275. doi: 10.11648/j.ijefm.20241205.14

Copy

|

Download

-

@article{10.11648/j.ijefm.20241205.14,

author = {Roshan Harshapriya},

title = {Diversification Effect of Gold as an Asset Class in Foreign Exchange Reserve Portfolio, Evidence from Sri Lanka

},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {12},

number = {5},

pages = {267-275},

doi = {10.11648/j.ijefm.20241205.14},

url = {https://doi.org/10.11648/j.ijefm.20241205.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20241205.14},

abstract = {Foreign Exchange Reserves of the countries play a major role in managing exchange rate and monetary policy, particularly in emerging countries as Sri Lanka. Therefore, it is important to manage foreign exchange reserves in an open and transparent manner with clear objectives of what is going to be achieved. For a country like Sri Lanka the main objective would be the safety of the assets since it is difficult to absorb substantial risks in managing foreign exchange reserves due to relative lower size compared to its exposure to external sector of the economy. When it comes to gold as an assets class is considered to safe-haven assets due to its nature of higher return in times of crisis and inflationary periods. The objective of this study is to explore the diversification impact of gold on foreign exchange reserves in Sri Lanka for the period from 2007 to 2023. To explore the impact of diversification, correlation between gold and existing foreign exchange reserves and additional excess return per unit of risk provide with the inclusion of gold into the portfolio were used to analyze the possible diversification impact. The results showed that there is an increase in excess return with the addition of 1% to 5% of gold as a percentage of total foreign exchange reserves, while correlation of gold with existing portfolio was less than 0.5 indicating diversification impact. Further, the Sharpe ratio was also seen increasing when the gold composition in foreign exchange reserve portfolio was increased. It was found that gold can be considered as an asset class which help diversification for foreign exchange reserves of Sri Lanka, even though the same are managed in very conservatively.

},

year = {2024}

}

Copy

|

Download

-

TY - JOUR

T1 - Diversification Effect of Gold as an Asset Class in Foreign Exchange Reserve Portfolio, Evidence from Sri Lanka

AU - Roshan Harshapriya

Y1 - 2024/09/20

PY - 2024

N1 - https://doi.org/10.11648/j.ijefm.20241205.14

DO - 10.11648/j.ijefm.20241205.14

T2 - International Journal of Economics, Finance and Management Sciences

JF - International Journal of Economics, Finance and Management Sciences

JO - International Journal of Economics, Finance and Management Sciences

SP - 267

EP - 275

PB - Science Publishing Group

SN - 2326-9561

UR - https://doi.org/10.11648/j.ijefm.20241205.14

AB - Foreign Exchange Reserves of the countries play a major role in managing exchange rate and monetary policy, particularly in emerging countries as Sri Lanka. Therefore, it is important to manage foreign exchange reserves in an open and transparent manner with clear objectives of what is going to be achieved. For a country like Sri Lanka the main objective would be the safety of the assets since it is difficult to absorb substantial risks in managing foreign exchange reserves due to relative lower size compared to its exposure to external sector of the economy. When it comes to gold as an assets class is considered to safe-haven assets due to its nature of higher return in times of crisis and inflationary periods. The objective of this study is to explore the diversification impact of gold on foreign exchange reserves in Sri Lanka for the period from 2007 to 2023. To explore the impact of diversification, correlation between gold and existing foreign exchange reserves and additional excess return per unit of risk provide with the inclusion of gold into the portfolio were used to analyze the possible diversification impact. The results showed that there is an increase in excess return with the addition of 1% to 5% of gold as a percentage of total foreign exchange reserves, while correlation of gold with existing portfolio was less than 0.5 indicating diversification impact. Further, the Sharpe ratio was also seen increasing when the gold composition in foreign exchange reserve portfolio was increased. It was found that gold can be considered as an asset class which help diversification for foreign exchange reserves of Sri Lanka, even though the same are managed in very conservatively.

VL - 12

IS - 5

ER -

Copy

|

Download